GST Portal Enhancements for GSTR 3B Filing 2026

Starting February 2026, the GST portal will improve GSTR 3B filing and IGST credit set-off processes. Discover key changes like flexible ITC utilization rules and increased automation for tax liabilities.

CA AMIT AGRAWAL

5/8/2024

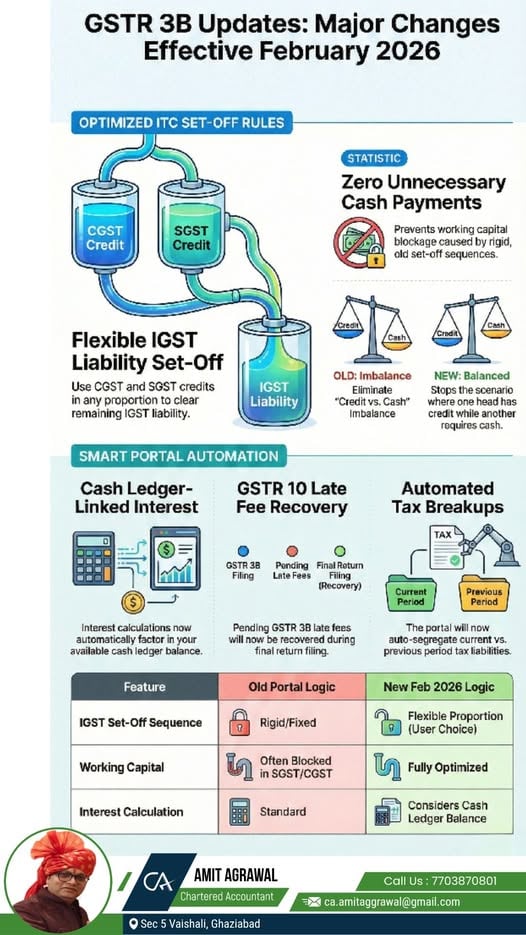

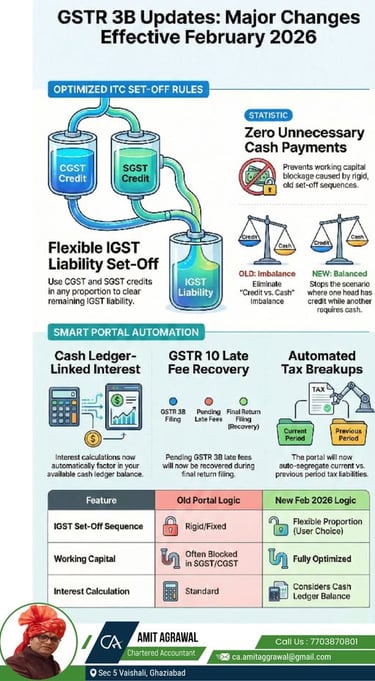

Managing GST compliance often feels like an exercise in forced inefficiency, particularly when a business is compelled to pay cash for one tax head while holding ample credit in another. For years, the rigidity of set-off rules has led to the frustration of "trapped" liquidity—where SGST credits sit idle while the taxpayer is forced to drain cash to settle CGST liabilities. However, a significant shift is coming: starting February 2026 (applicable to the January 2026 returns), the GST portal is receiving a "smart" architectural upgrade designed to optimize working capital and drastically reduce the risk of tax notices.

1. The "Any Proportion" Rule: Unblocking Your Working Capital

The most significant relief for businesses is the overhaul of the IGST set-off mechanism. Under the current rigid framework, the sequence of utilizing Input Tax Credit (ITC) often leads to unutilized Input Tax Credit (ITC) accumulation in one bucket while requiring cash outflows in another.

The new "smart" logic follows a two-step sequence that prioritizes liquidity. First, any IGST liability must be wiped out using the available IGST credit. Once the IGST credit is exhausted, if a liability remains, the taxpayer now has the absolute freedom to utilize CGST and SGST credits in any proportion to settle the balance.

Consider the strategic value: Previously, if you had a remaining IGST liability, the system often forced a set-off against CGST first. If your CGST credit was then exhausted, you might have been forced to pay your regular CGST liability in cash, even if you had a massive surplus of SGST credit carrying forward. By allowing you to choose the ratio—for example, using more SGST credit to cover the IGST gap—the portal ensures you can protect your cash flow and avoid "unnecessary working capital blockage."

"In any portion, I will be able to use C and S... so that unnecessary working capital is not blocked and I can pay as much as I want from C and as much as I want from S."

2. Smart Interest: The Portal Finally Respects Your Cash Ledger

The GST portal is transitioning from a static calculator to a dynamic system that aligns its logic with the taxpayer’s actual liquidity position. The system will now automatically calculate interest by factoring in the minimum balance available in the Electronic Cash Ledger during the period of delay.

This is a game-changing synthesis of tax law and fintech logic. Historically, the portal might calculate interest on the full liability regardless of the funds sitting in your ledger. The "Smart Portal" now acknowledges a fundamental truth: cash in the ledger is money already paid to the government. By considering this minimum balance, the system ensures that interest is only levied on the actual shortfall. This removes human error and ensures that the interest burden is fair, transparent, and reflective of the taxpayer’s real-time financial standing.

3. The GSTR 10 Trap: Closing the Compliance Loop

For businesses looking to cancel their registration, the portal is introducing a "closing the loop" mechanism through tighter integration between GSTR 3B and the Final Return (GSTR 10). If a taxpayer’s last GSTR 3B filing was delayed, the associated late fees will now be automatically recovered during the filing of GSTR 10.

While this may seem like stricter enforcement, it is a strategic advantage for the taxpayer. By automating this recovery at the point of the final return, the system mitigates the risk of non-compliance during the cancellation process. It effectively prevents future litigation or the arrival of surprise recovery notices from GST officers years after a business has ceased operations. It ensures a clean exit from the GST ecosystem.

4. Precision Reporting: Distinguishing the Past from the Present

The update to Table 6.1 introduces a level of granularity that will redefine audit readiness. Driven by the "Date of Invoice" reported in GSTR 1, the portal will now automatically separate "current period" liability from "previous period" liability within a single GSTR 3B return.

As a consultant, I view this as a vital tool for precision. This breakup allows the portal to calculate interest with pinpoint accuracy, as it can distinguish exactly when a liability was incurred versus when it is being reported. For the taxpayer, this creates a robust, date-stamped audit trail. This transparency makes it significantly easier to reconcile records and respond to departmental inquiries with data-backed confidence.

Conclusion: The Era of "Notice-Free" Compliance?

The overarching theme of these 2026 updates is a push toward total automation and the elimination of the "delta" between taxpayer reporting and officer assessment. When the portal calculates interest, set-off ratios, and late fees correctly at the point of filing, it leaves no room for manual discrepancies that typically trigger a GST officer to issue a recovery notice.

By handling these complexities at the source, the system aims to make the January 2026 tax period the beginning of a more seamless, intervention-free era. As the portal takes over the heavy lifting of compliance logic, the margin for error shrinks.

This leads to a broader question for the future of fintech: what other manual bottlenecks in the GST lifecycle do you believe should be automated next to further empower business owners?

CA Amit Agrabal – Professional Insights

Explore our sleek website template for seamless navigation.

Contact

Newsletter

caamitagrabal@gmail.com

7703870801

© 2026. All rights reserved.